Table of contents

- What Is Blockchain Technology?

- Why is Blockchain Popular?

- Key Elements of a Blockchain

- How Does Blockchain Technology Work?

- Types of Blockchains

- History of Blockchain

- Pros and Cons of Blockchain

- The Implications of Blockchain Technology

- A Future With Blockchain Technology

- Try AtomicDEX — Hold and Trade Cryptocurrencies

Table of contents

- What Is Blockchain Technology?

- Why is Blockchain Popular?

- Key Elements of a Blockchain

- How Does Blockchain Technology Work?

- Types of Blockchains

- History of Blockchain

- Pros and Cons of Blockchain

- The Implications of Blockchain Technology

- A Future With Blockchain Technology

- Try AtomicDEX — Hold and Trade Cryptocurrencies

A blockchain is a distributed ledger that shares transactions across computers on a network without any possibility of alterations after the transaction is processed by the network.

Blockchain technology has changed the way people view everything from financial processes to secure storage. Since its inception, blockchain has brought about a significant shift from traditional finance to a more decentralized system.

In traditional finance, most operations are centrally controlled, with single entities exercising total authority. This centralization has given rise to many financial regulations that are compulsory for all participants to follow. Blockchain technology helps solve this problem by giving users total control over their assets and the networks they interact on.

What Is Blockchain Technology?

Blockchain technology includes a distributed database that allows for secure, transparent, and tamper-proof data storage and transmission. Rather than having a central entity manage the database as with traditional financial institutions, blockchain technology validates and stores transactions via a decentralized peer-to-peer network of computers.

This decentralized approach to managing transaction data has many potential benefits. For instance, it improves data security since there is no central server that hackers can target. Additionally, it supports transparency since all transactions are publically available on the blockchain. Finally, blockchain tech facilitates near-instantaneous transaction settlements by eliminating the need for third-party intermediaries to process interactions.

Why is Blockchain Popular?

Blockchains are digital ledgers that have become very popular because they address many of the issues traditional financial systems face. Some of these include data security, centralized control, and transaction speed. Other reasons for blockchain's popularity include the following:

- Secure end-to-end encrypted digital currency transactions that promote crypto decentralization

- Complete control of funds with no limitations on large transactions

- Near instant and efficient transaction processing with no central authority

- Transparent access to digital records

- Seamless cross-border transactions

Key Elements of a Blockchain

The following are key elements of blockchain networks:

Distributed Ledger Technology

All blockchains are digital ledgers of transactions distributed across a network of computers (known as nodes). These distributed ledgers use each independent node on the network to record, share, and synchronize transactions instead of keeping them on a singular centralized server. In addition to a distributed ledger, blockchains use other technology like digital signatures, distributed networks, encryption, and decryption.

Immutable Records

Data immutability is another crucial element of a blockchain. This feature ensures that once committed, no transaction can be canceled, reverted, or altered. Immutability is one of blockchain's most definitive features and is responsible for detecting and avoiding duplicate or fraudulent transactions.

Smart Contracts

Smart contracts enable the near-instant execution of transactions on a blockchain. These contracts are self-executing digital agreements that allow two or more parties to exchange assets over blockchain networks and execute the terms of a predefined contract. However, like any other software code, smart contracts sometimes have security loopholes. Therefore, performing smart security contract audits is necessary to identify and eliminate possible vulnerabilities. Not every blockchain requires smart contract integration, such as the Bitcoin protocol.

How Does Blockchain Technology Work?

A blockchain network combines the functions of cryptographic keys and a peer-to-peer network containing a distributed ledger of transactions. Cryptographic keys consist of private and public keys that help to execute transactions between two parties and create a secure digital identity reference on a network. This secure identity, known as a 'digital signature,' is responsible for user authorization and transaction control.

The digital signature works with a peer-to-peer network, a collection of participants that act as authorities and use the signature to reach a consensus. When verified, the transaction is stored in a data block that forms a chain by linking to previous transactions. The entire network then distributes this chain of blocks, ensuring that all nodes have a copy of the latest transaction history.

Types of Blockchains

There are four main types of blockchains:

Private Blockchain Networks

Private blockchains operate in a closed network and work well for private organizations and businesses. By maintaining a restricted network, users can control a participant's access by setting different parameters.

Public Blockchain Networks

A public blockchain network is permissionless, allowing anyone to access and perform transactions. It is a non-restrictive network where each node has a copy of the entire ledger. This also means that anyone with an active internet connection can access and utilize a public blockchain.

Permissioned Blockchain Networks

Permissioned blockchain networks are not accessible to all members of the general public. Only users with permissions can perform transactions on this type of blockchain after an identity verification process. Ledger administrators and centralized nodes control permissioned blockchain networks by granting access to specific users and managing the exact actions they can perform.

Consortium Blockchains

Multiple organizations manage a consortium blockchain network. This type of blockchain combines public and private elements since it comprises a group of private blockchains that share information. Therefore, consortium blockchains are ideal for collaboration between multiple organizations.

History of Blockchain

The growth of blockchain tech began in 1991 when Stuart Haber and W Scott Stornetta published a paper describing the use of cryptography to link blockchains and timestamp documents. The current blockchain concept became popular after an unknown person, entity, or group known as Satoshi Nakamoto made the introduction of Bitcoin in 2008.

Following the release of a 2008 whitepaper on the subject, Nakamoto developed the first blockchain network in 2009 as the public ledger for the Bitcoin cryptocurrency. The technologies and concepts around blockchains have continued to evolve, bringing about the various centralized and decentralized blockchain services known today.

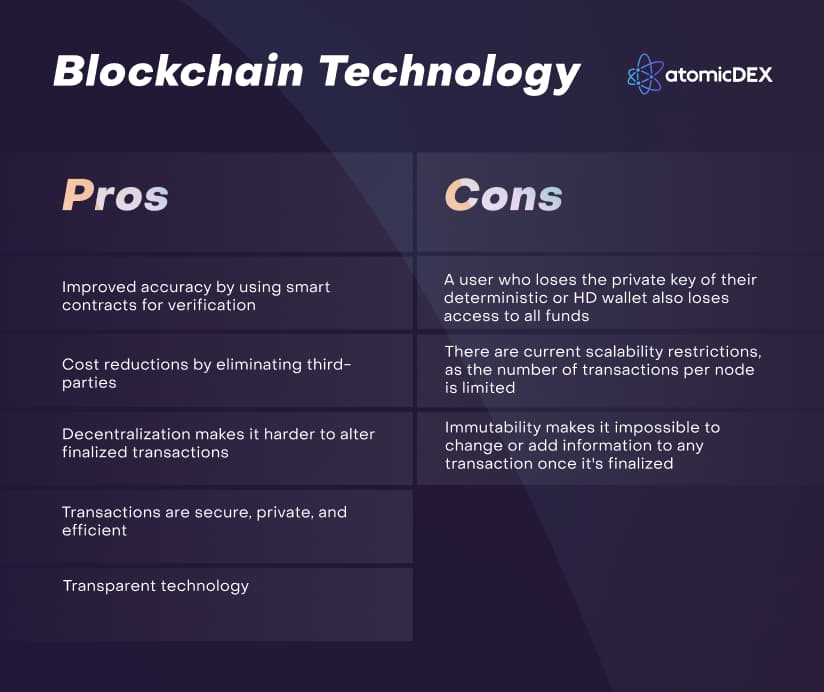

Pros and Cons of Blockchain

There are several pros and cons to blockchain usage, as with all other forms of technology. The following are some of the most common:

The Implications of Blockchain Technology

The implications of blockchain technology are evolving. With enough support and adoption, blockchain technology could considerably reduce dependence on intermediaries such as commercial banks and centralized financial institutions. Blockchain technology could also revolutionize many other sectors.

For example, the technology could streamline tedious processes and reduce costs in the finance industry. For supply chain transactions, blockchain can help quality control by improving product traceability and reliability. The healthcare sector can also benefit by using blockchain to securely store and share patient data, with the patient only making aspects of their medical data available as needed.

A Future With Blockchain Technology

Besides its current use with cryptocurrencies and NFTs, blockchain has the potential to improve people's interactions with the digital world. Blockchain can change how people do business, govern, and socialize.

It can make contracts into law, and make transactions much more efficient by automating many processes using smart contracts. Blockchain tech can also power databases for secure medical records, birth certificates, and voting results by providing tamper-proof data storage and cryptographic verification.

Try AtomicDEX — Hold and Trade Cryptocurrencies

As blockchain technology evolves, more cryptocurrencies with growth possibilities will emerge.

Users can set up an AtomicDEX wallet to hold and trade both well-known cryptocurrencies as well as emerging cryptocurrencies all from one app.

Related articles

See all articles

How to Buy Land in the Metaverse

Metaverse land: a new frontier for investors. Discover the exciting possibilities, platforms, and factors to consider before purchasing virtual real e ...

Exploring dApp Browsers: Definition, Features, and Benefits

Read this post to get an in-depth overview of common dApp browser features, the importance of dApp browsers in the blockchain ecosystem, and how to us ...

What are Tokenomics?

Tokenomics, a shortened wording of 'token economics refers to use cases as well as the supply and demand of a given cryptocurrency. Read on to learn m ...

See all news